Binomial Tree, Cox-Ross-Rubinstein, Method¶

Overview¶

The Cox-Ross-Rubinstein Binomial Tree method is an instance of the Binomial Options Pricing Model (BOPM) , published originally by Cox, Ross and Rubinstein in their 1979 paper “Option Pricing: A Simplified Approach” [CRR1979].

In this method, the binomial tree is used to model the propagation of stock price in time towards a set of possibilities at the Expiration date, based on the stock Volatility. For “N” time steps into which the model scenario duration is subdivided, there are N+1 possible stock prices at the expiration time.

Based on the N+1 Call or Put Option values at expiration, option values are backward-propagated to the initial time using step probabilities and the interest-rate, to obtain the Call or Put Option price. Comparing intermediate Call/Put values during back-propagation to stock prices allows American Option prices to be calculated.

Cox-Ross-Rubinstein show that as N tends to ∞, the binomial European Put/Call solutions tend towards the Black-Scholes solutions. (Both models make the same underlying assumptions.) In an example where K = $35.00 and N = 150, they show the difference is less than $0.01.

In a later paper, Leisen & Reimer [LR1995] propose a method to increase the convergence speed of the CRR binomial lattice to converge faster.

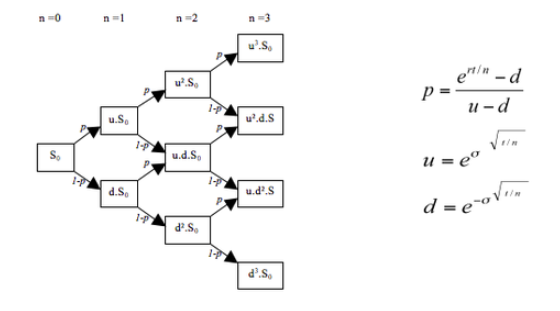

The diagram above shows an example of a binomial tree, where the number of time steps is \(n\). (Note that \(n\) steps results in \(n + 1\) separate propagated \(S\) values after the n-th step.)

At each step the initial stock price \(S_0\) is propagated in an Up path and a Down path from each node, with Up and Down factors \(u\) and \(d\). The “Up” probability is \(p\); Down is \(1 - p\).

The equations in the diagram show the derivation, where \(\sigma\) is the stock volatility, \(r\) the “risk-free rate”, \(t\) the scenario duration and \(n\) the number of time steps. The dividend yield in the above is assumed to be zero and not included in the expression for \(p\), but may be included when required.

(Diagram source: Wikipedia article Binomial Options Pricing Model (BOPM) .)

References¶

| [CRR1979] | Cox, J. C., Ross, S. A., Rubinstein, M., “Option Pricing: A Simplified Approach”, Journal of Financial Economics (1979) |

| [LR1995] | Leisen, D., Reimer, M., “Binomial Models for Option Valuation - Examining and Improving Convergence”, Rheinische Friedrich-Wilhelms-Universität, Bonn, (1995). |